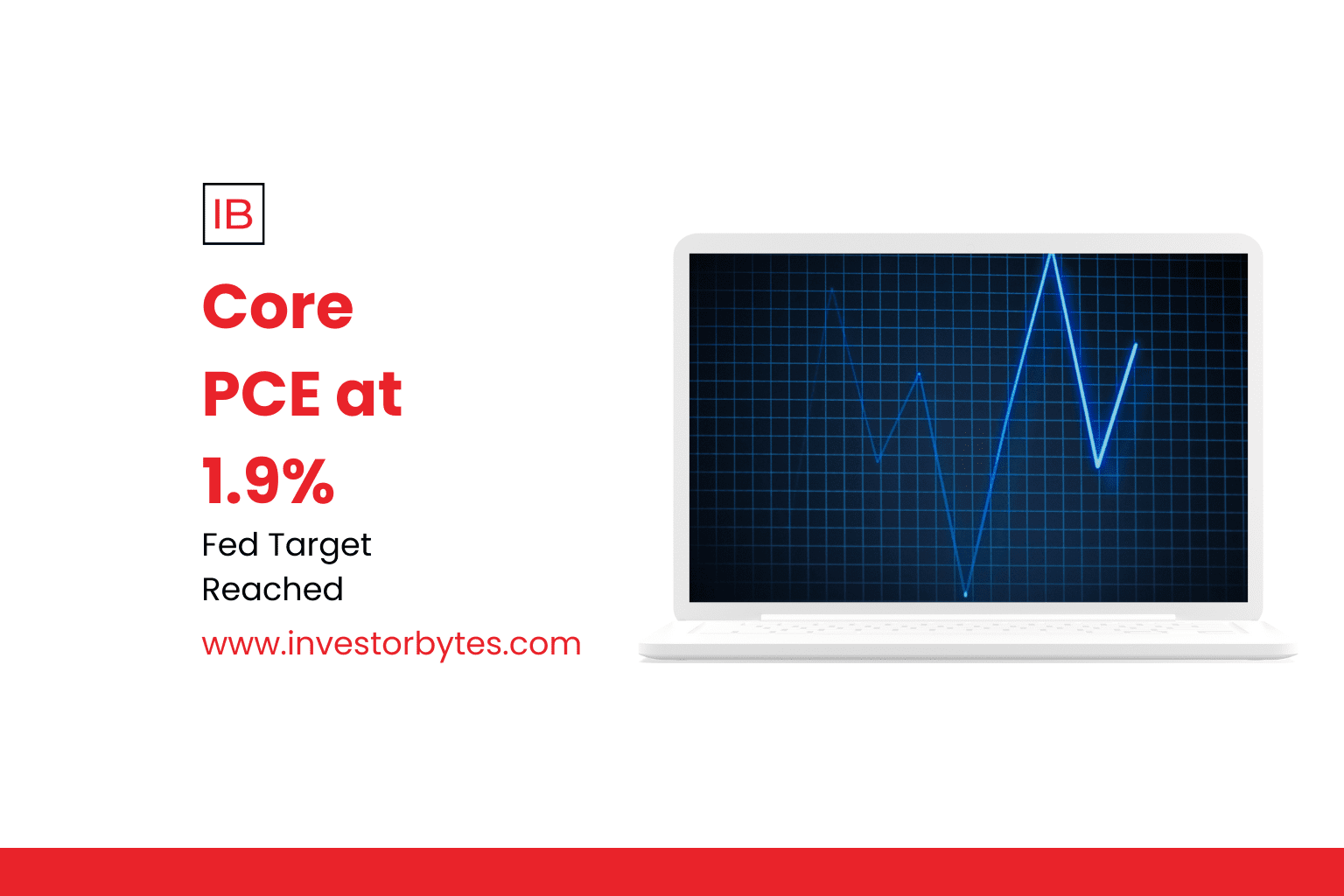

The core PCE price index, the Federal Reserve’s North Star for inflation, cooled to 1.9% year-over-year in November 2025, a notch below October’s 2.0% and the lowest since February 2021, underscoring a trajectory of ebbing price pressures despite tariff headwinds and robust consumer spending. This monthly whisper—down from August’s 2.9% peak—excludes volatile food and energy, spotlighting underlying trends in services (up 0.2% month-over-month) and durable goods (flat), as per Bureau of Economic Analysis data released December 5 amid the post-shutdown data deluge.

Fed Chair Jerome Powell hailed the print as “encouraging,” affirming a 25-basis-point December cut’s 90% probability via CME FedWatch, with projections for two more in 2026 to sustain 2% equilibrium. Headline PCE held at 2.8%, buoyed by gasoline’s 5% dip, yet core’s sub-2% breach—first since 2021—eases stagflation specters, with Cleveland Fed nowcasts eyeing 1.8% by Q1 2026. Market ripples ensued: Treasury yields tumbled 5 basis points to 4.15% on the 10-year, equities notched fractional gains, and the dollar softened 0.3% versus majors.

This disinflationary pivot, fueled by supply-chain mends and AI efficiencies curbing input costs, contrasts 2022’s 7% zenith, empowering fiscal space for infrastructure amid $11 billion shutdown scars. For households, real purchasing power swells—disposable income up 0.4%—yet vigilance persists on shelter inflation (3.2%) and wage spirals (4.1%). As PCE supplants CPI for behavioral nuance, 1.9% cements the Fed’s pivot, potentially unlocking $2 trillion in pent-up capex.