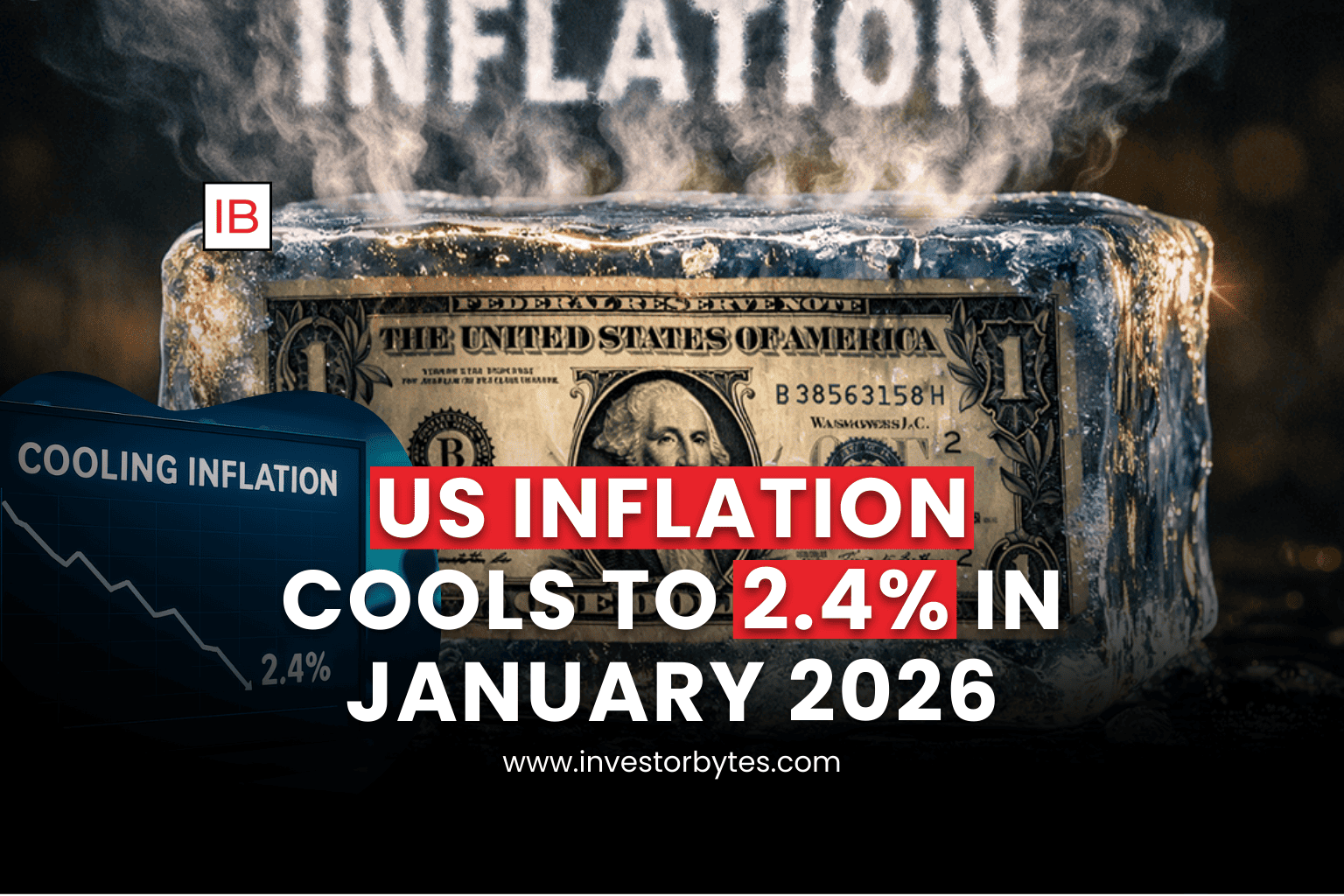

U.S. Bureau of Labor Statistics reported that the annual inflation rate slowed to 2.4% in January, reaching its lowest level since May 2025 and beating economist forecasts of 2.5%.

The report marks a “slow glide” toward the Federal Reserve’s target, primarily driven by sharp declines in gasoline and used vehicle prices. Despite this cooling trend, Core CPI (which excludes volatile food and energy) remained somewhat sticky at 2.5%, suggesting that while the “inflation fever” has broken, certain service-sector costs remain elevated.

January 2026 CPI: Key Drivers

The deceleration from December’s 2.7% rate was largely credited to energy relief and specific grocery categories, though shelter and certain meats remain expensive.

Energy Relief: Gasoline prices plunged 7.5% year-over-year, providing the most significant downward pressure on the headline figure.

Grocery Mixed Bag: While overall food inflation slowed to 2.1%, households saw a dramatic 34.2% drop in egg prices compared to the avian-flu-impacted highs of 2025. Conversely, ground beef (+17.2%) and coffee (+18.3%) prices continued to surge.

Shelter & Services: The shelter index rose 3.0% annually, showing a steady cooling from the 8% peaks of the pandemic era. However, “supercore” inflation (services minus housing) saw a monthly jump of 0.6%, driven by rising airfares and medical care.

| Metric | January 2026 (YoY) | Change from Dec 2025 |

| Headline CPI | 2.4% | -0.3% |

| Core CPI | 2.5% | -0.1% |

| Gasoline | -7.5% | Significant Decline |

| Shelter | 3.0% | Moderating |

The Fed’s Dilemma

The cooling inflation data comes on the heels of a surprisingly strong January jobs report, which saw 130,000 jobs added and unemployment tick down to 4.3%.

Rate Cut Outlook: While the 2.4% print is “reassuring,” analysts believe the Fed will likely hold interest rates steady at its mid-March meeting (currently at 3.50% – 3.75%).

Wait-and-See: Policymakers are wary of “running the economy too hot” with preemptive cuts, especially as the Trump administration’s tariff policies continue to fluctuate, potentially impacting future goods prices.

Market Reaction: U.S. equity futures turned positive following the release, and the 10-year Treasury yield declined as investors bet on “normalization” cuts potentially beginning in June 2026.