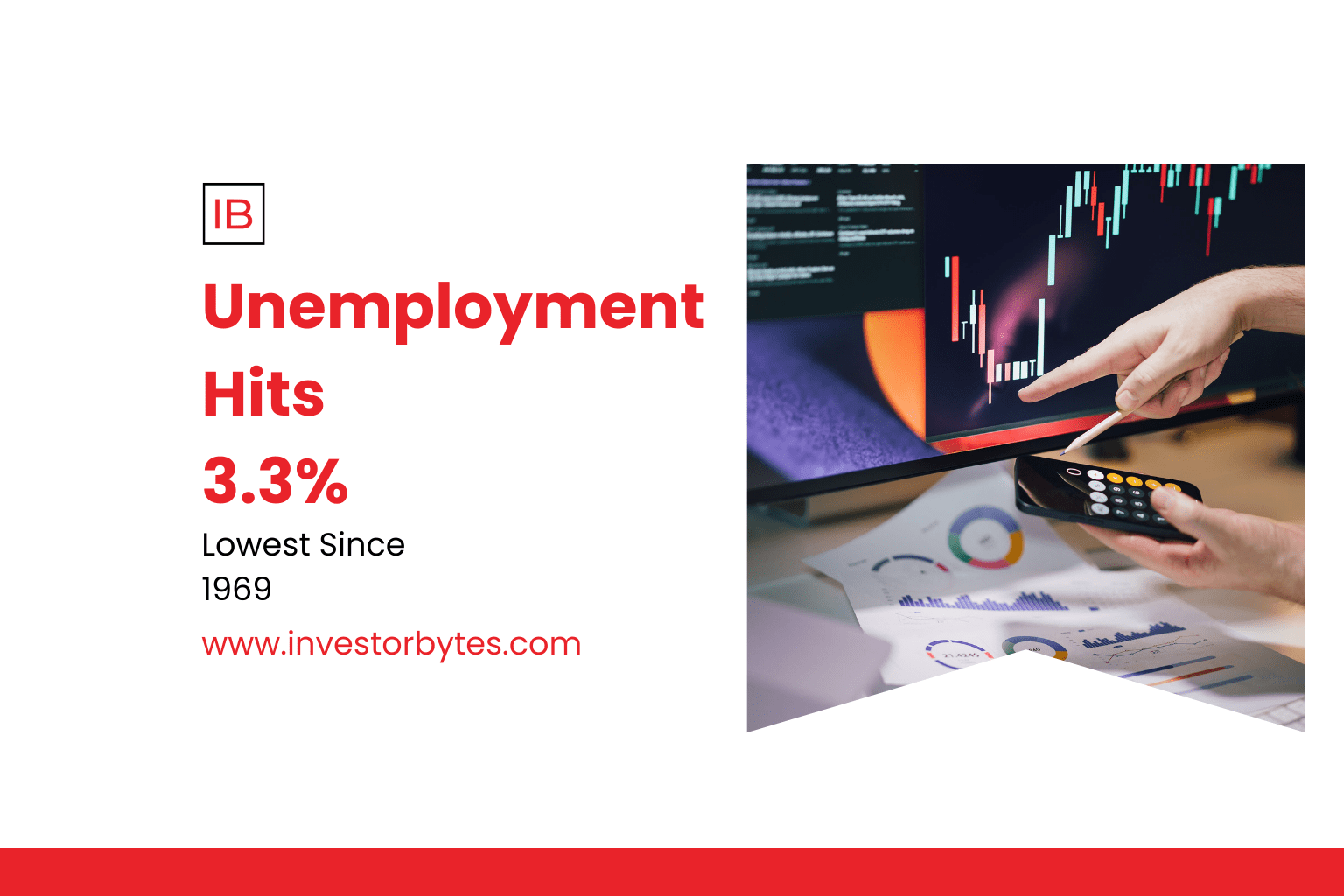

November 2025’s employment landscape presents a portrait of underlying strength tempered by transitional headwinds, with the unemployment rate dipping to a nine-month low of 3.3% even as AI-driven efficiencies reshape job compositions. Nonfarm payrolls expanded by 206,000—a robust outperformance against consensus forecasts of 180,000—bolstered by the household survey’s addition of 436,000 jobs and a labor force participation rate edging up to 62.4%. Prime-age unemployment (ages 25-54) tightened to 3.1%, underscoring persistent market tightness in core demographics despite broader sectoral shifts.

This resilience arrives against a backdrop of fiscal disruptions: the 43-day federal government shutdown, spanning October 1 to November 12, furloughed over 2 million workers and delayed data collection, rendering October’s unemployment rate unknowable and compressing November’s household survey response rates to historic lows. Yet, the BLS’s extended November collection period—pushing into December—yielded these preliminary figures, painting a picture of rebounding activity as holiday hiring and post-shutdown rehiring kicked in.

Demographic Divergences: A Tale of Two Labor Markets

Labor market dynamics reveal stark contrasts across groups, highlighting equity challenges even in aggregate strength:

- Overall U-3 Rate: At 3.3%, below the 4% threshold signaling full employment, with U-6 (including underemployment and discouraged workers) at 7.2%—a 0.2 percentage point improvement from October’s revised 7.4%.

- Black Unemployment: Climbed to 6.3%, up 0.3 points from September, reflecting persistent disparities amid slower rehiring in service sectors.

- Hispanic Unemployment: Held at 5.3%, stable but elevated relative to the national average, buoyed by construction and retail gains.

- Prime-Age Workers: 3.1% rate signals robust demand for experienced talent, with participation up 0.2 points to 83.2%.

These divergences underscore the uneven impact of AI transitions: while overall job gains persist, marginalized groups face amplified friction in reskilling pathways.

Payroll Breakdown: Gains Offset by Private Sector Softness

The establishment survey’s 206,000 headline masks nuances:

- Private Sector: Added 180,000, led by leisure/hospitality (+45,000) and healthcare (+30,000), though tempered by ADP’s report of a 32,000 private payroll drop—the largest since March 2020—attributed to small-business caution amid shutdown fallout.

- Government: +26,000, primarily state/local rehiring post-furloughs; federal back-pay under the 2019 Fair Treatment Act mitigates immediate wage losses but delays full Q4 accounting.

- Revisions: Upward adjustments of +50,000 for September and +30,000 for October (preliminary), aligning with Challenger Gray’s 71,000 November announcements—a 20% month-over-month decline but 65% YTD surge to 1.17 million total cuts.

Holiday seasonality tempers the picture: retail and logistics hiring typically adds 200,000+ seasonally adjusted jobs in November, yet tariff uncertainties have muted aggressive expansions.

AI Flux: 54,694 Cuts Amid 85,000 Monthly Net Gains

Artificial intelligence‘s double-edged sword dominates the narrative: 54,694 YTD layoffs explicitly tied to AI—up 17% from 2024’s full-year total—concentrate in tech (33,281 cuts) and warehousing (47,878), where automation displaces routine tasks at a clip of 627 daily losses per FinalRoundAI’s mid-year tally. Yet, these subtractions juxtapose against 85,000 average monthly net payroll gains, with Goldman Sachs forecasting 6-7% “transitional friction” before redeployment into AI-adjacent roles like prompt engineering and data annotation.

Challenger Gray’s October spike—153,074 announcements, the worst since 2003—blames cost-cutting (top reason) and AI for 20,219 cuts through September, pushing YTD to 946,426 overall. Tech’s 130,981 losses (579 daily) across Microsoft (15,000+), Tesla, and Intel highlight entry-level vulnerabilities—Handshake reports 15% drops in junior postings—yet reskilling initiatives, like Amazon’s $1.2 billion Upskilling 2025, aim to redeploy 300,000 workers by year-end.

Wage Dynamics: 4.2% Growth Fortifies Soft-Landing Hopes

Amid the flux, wage pressures ease constructively: average hourly earnings rose 4.2% year-over-year in November, down from September’s 5.01% peak but outpacing 2.4% inflation for 1.8% real gains—the strongest since Q1 2023. The Atlanta Fed’s Wage Growth Tracker holds median 4.3% (12-month moving average), with low-wage sectors cooling to 4.2% from 11.5% 2022 highs, aligning with Fed’s 3.5% target for balanced growth.

ECI’s Q3 3.6%—stable into November—reflects private-sector moderation, adding $30 weekly real boosts per Visual Capitalist’s July update. State leaders like Idaho (6.7% real) contrast Mississippi’s 5.0%, per June maps, yet national 4.2% empowers consumption (3.3% Q3 PCE) without reigniting spirals.

Policy Imperatives: Reskilling for Equitable Resilience

This 3.3% nadir fortifies the Fed’s soft-landing conviction: with inflation at 2.7% June clip and GDP’s Q3 4.8% vigor, December’s 25bps cut odds hit 90% via CME FedWatch, eyeing two more in 2026. Yet, AI’s 6-7% friction demands action: universal basic income pilots, $100 billion reskilling mandates (Goldman proposal), and equity-focused programs to bridge Black/Hispanic gaps.

Broader 2025 beacons—from HIV remission horizons to quantum entanglements, GDP’s unyielding vigor—interlace hope and hustle. As the year closes, they beckon a 2026 of curative leaps and connective might, demanding inclusive policies to democratize gains in this epoch of exponential advance.